Tax-Deferred Triumph: Section 1031 Exchange and Its Impact on Real Estate Investment

Real estate investment is lucrative, but the tax implications can often hinder maximizing returns. Enter Section 1031 Exchange, a powerful tool that allows investors to defer capital gains taxes when selling and reinvesting in like-kind properties. In this article, we delve into the intricacies of Section 1031 and its transformative impact on real estate investment.

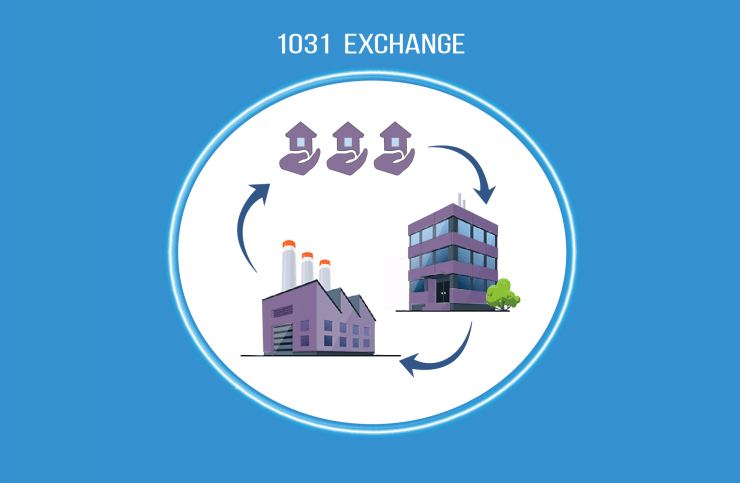

2. Understanding Section 1031 Exchange

Section 1031, also known as a like-kind exchange, is a provision in the U.S. Internal Revenue Code that allows investors to defer capital gains taxes on the sale of qualifying properties. The fundamental idea is that if an investor reinvests the proceeds from the sale into another property of equal or more excellent value, the taxes on the capital gains are postponed.

3. The Mechanics of a Section 1031 Exchange

To successfully execute a Section 1031 Exchange, investors must adhere to specific guidelines. The process involves identifying a replacement property within 45 days of selling the original parcel and completing the purchase within 180 days. The replacement property must be of equal or more excellent value, and the equity from the relinquished property must be fully reinvested.

4. Benefits and Advantages

The advantages of Section 1031 Exchange are manifold. By deferring capital gains taxes, investors have more capital to reinvest, enabling the growth of their real estate portfolios. This tax deferral can be especially advantageous for those looking to upgrade or diversify their holdings without the burden of immediate tax liabilities.

5. Risks and Considerations

While Section 1031 Exchange offers substantial benefits, being aware of the associated risks is essential. Market conditions, property identification constraints, and failure to meet strict timelines can pose challenges. Investors should carefully weigh these factors and seek professional guidance to navigate potential pitfalls successfully.

6. Real-world Applications

The application of Section 1031 Exchange is not limited to specific real estate types. Investors across various sectors can leverage this provision, from residential properties to commercial real estate, to optimize their tax positions. The flexibility of like-kind exchanges opens the door for diverse investment strategies.

7. Legislative Changes and Future Outlook

Over time, legislative changes have influenced the landscape of Section 1031 Exchange. Understanding these modifications is crucial for investors to adapt and make informed decisions. Additionally, considering the current political and economic climate provides insights into the future viability of this tax-deferral strategy.

8. The Power of Tax Deferral: A Case Study

Explore a detailed case study illustrating the

potential impact of Section 1031 Exchange on a hypothetical real estate investor. Understand how the deferral of capital gains taxes can amplify the growth and profitability of the investment portfolio.

9. Conclusion: Unleashing the Potential of Section 1031

Section 1031 Exchange emerges as a game-changer for real estate investors in this tax-deferred triumph. By navigating the intricacies of like-kind exchanges, investors can strategically manage their tax liabilities, fueling the expansion and optimization of their property portfolios. The ability to defer capital gains taxes empowers investors to make more agile and lucrative investment decisions.

10. Frequently Asked Questions (FAQ)

Q1: What types of properties qualify for a Section 1031 Exchange?

A1: All real estate properties can qualify for a Section 1031 Exchange, including residential, commercial, and vacant land. The critical requirement is that the properties involved must be of like kind.

Q2: Can the replacement property be located anywhere in the United States?

A2: The replacement property can be located anywhere in the United States. Section 1031 Exchange does not restrict the geographical location of the properties involved.

Q3: Are there time constraints for identifying and acquiring replacement properties?

A3: Yes, strict timelines are involved in a Section 1031 Exchange. Investors have 45 days to identify potential replacement properties and 180 days to complete the purchase of the chosen replacement property.

Q4: What happens if the investor cannot identify a replacement property within 45 days?

A4: The exchange may be at risk if the investor fails to identify a replacement property within the specified 45-day period. It is crucial to work with qualified professionals to ensure compliance with these timelines.

Q5: Are there any limits on the number of properties involved in a like-kind exchange?

A5: Section 1031 Exchange does not limit the number of properties that can be involved in an exchange. However, each property must meet the like-kind requirement, and the total value of the replacement properties must equal or exceed the relinquished property’s value.

Q6: How has recent legislation affected Section 1031 Exchange?

A6: Legislative changes can impact Section 1031 Exchange rules. It is advisable to stay informed about any recent amendments to the tax code and seek professional advice to adapt strategies accordingly.